Last week, Wall Street put on a performance that could only be described as a master class in volatility—if your idea of a master class includes a hefty dose of uncertainty, courtesy of tariff theatrics. Major indexes took a beating on Thursday, with the S&P 500 falling 1.4% to 5,521.52, the Dow dipping 1.3% to 40,813.57, and the NASDAQ losing 2% to 17,303.01, officially entering correction territory for the first time since 2023.

Of course, nothing says “investor confidence” like doubling tariffs on Canadian steel and aluminum to 50%, which left even the most hardened market strategists chuckling in disbelief. The unpredictable trade antics set off a chain reaction that saw weekly declines of about 4.3% for the S&P 500 and 4.9% for the NASDAQ—even though a brief rally on Friday tried (and failed) to erase the damage.

At the end of the day, if investors needed a reminder that stability is an elusive myth in today’s economic climate, last week delivered it with a side of sarcasm and plenty of raw data. Does the recovery kick in before the next tweet sends the market spiraling once more?

Short-term market outlook

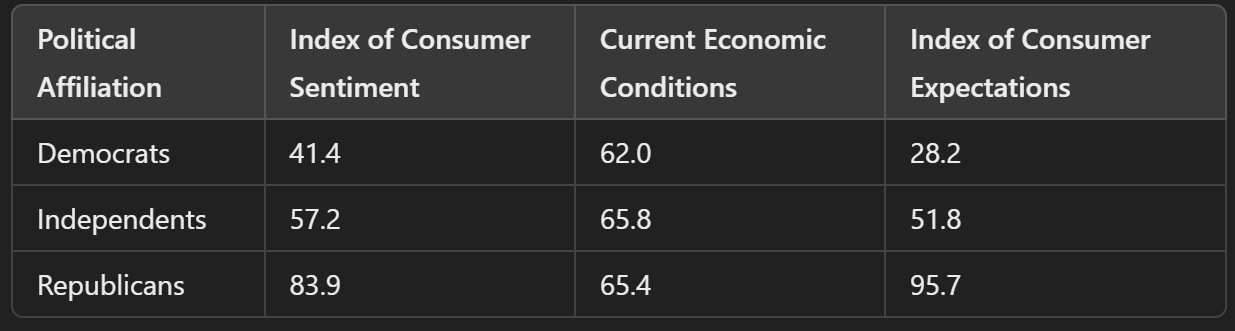

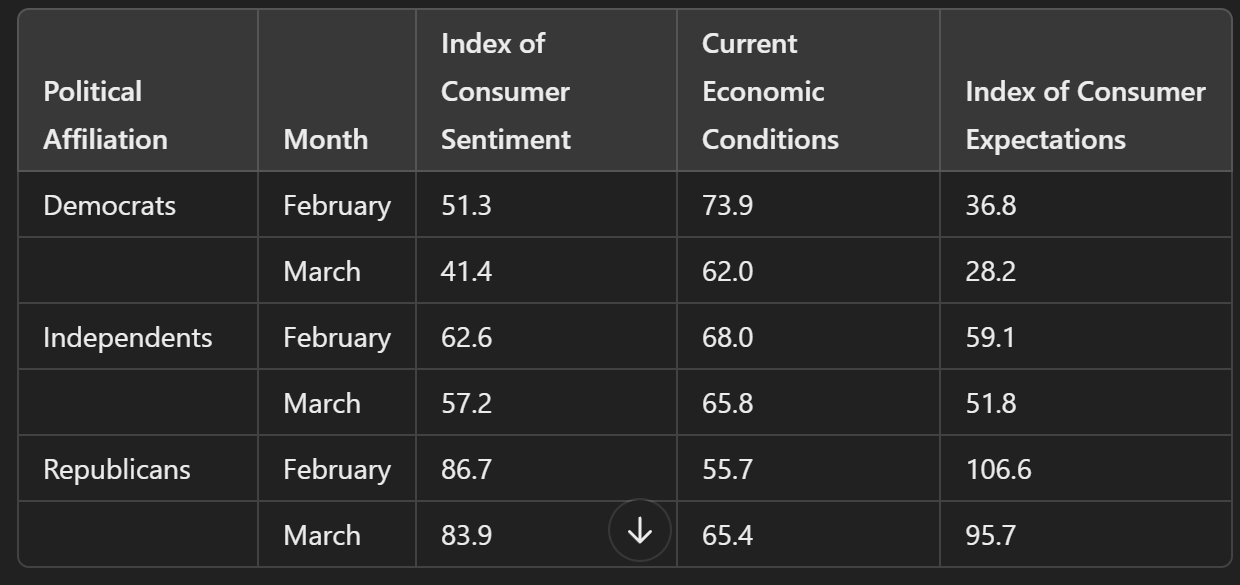

Consumer sentiment shows a considerable slowing. But the sentiment is very split depending on the political party.

However, there is a key distinction that’s important to recognize. While it’s still early, I place greater emphasis on a report I’ll discuss later in this article, which directly impacts corporate spending and hiring (Business Roundtable). If corporations aren’t spending, they aren’t hiring. Without hiring, consumers lack jobs, and without jobs, they have no money to spend. This report serves as an important leading indicator because it could potentially influence spending down the line. The following report shows how Republican, Democrat and Independent consumers feel about the current economy.

It’s worth noting that this potential weakness in consumer sentiment has not yet impacted economic activity. Economists monitor this closely because consumer attitudes influence spending. So far, unemployment remains stable but is showing signs of softening, while hiring and new job creation are falling short of necessary levels. In the short term, the trend appears to be shifting downward.

Current DOGE estimates suggest that approximately 300,000 federal workers could face layoffs. Additionally, the Brookings Institute estimates that for every federal worker, there are two contract workers, further amplifying the potential impact. Combined with the possibility of tariffs on Mexico and Canada, these factors significantly influence consumer sentiment, as many households—either directly or indirectly—are affected by government layoffs and the resulting trickle-down effects on their industries.

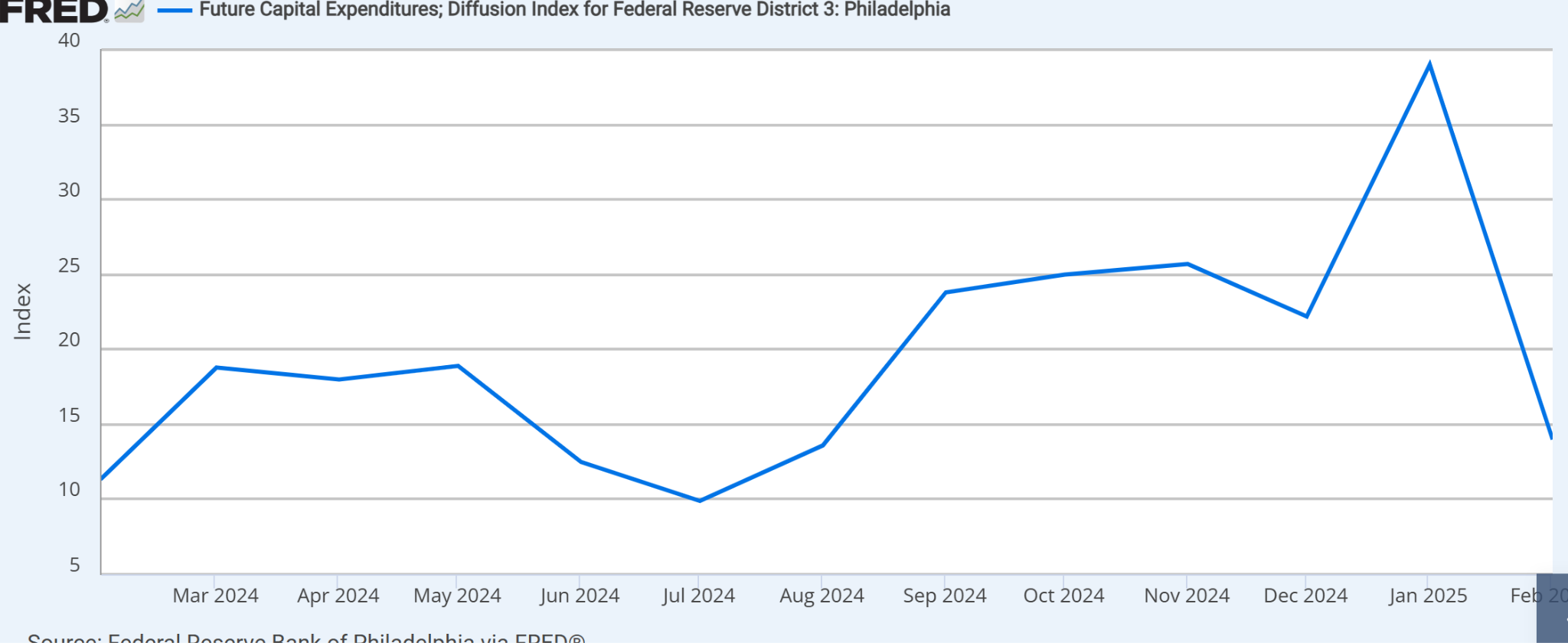

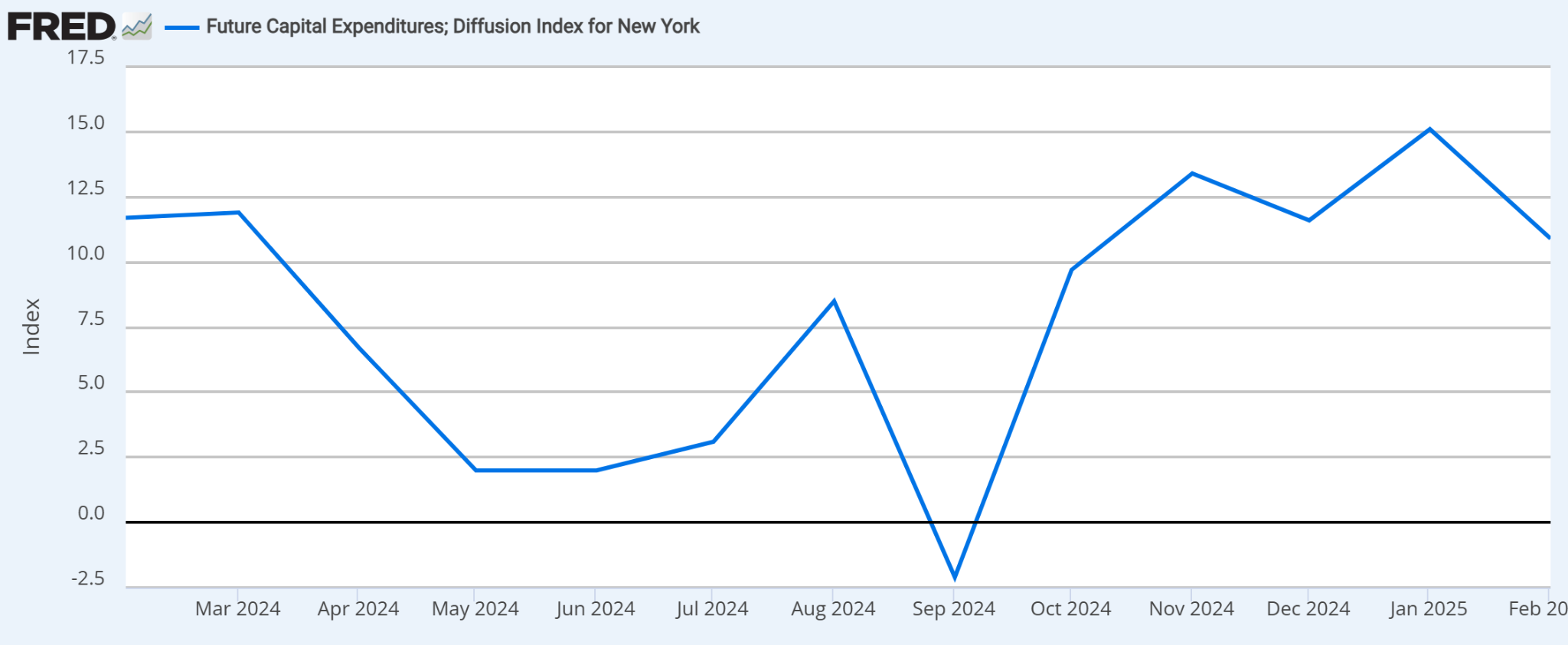

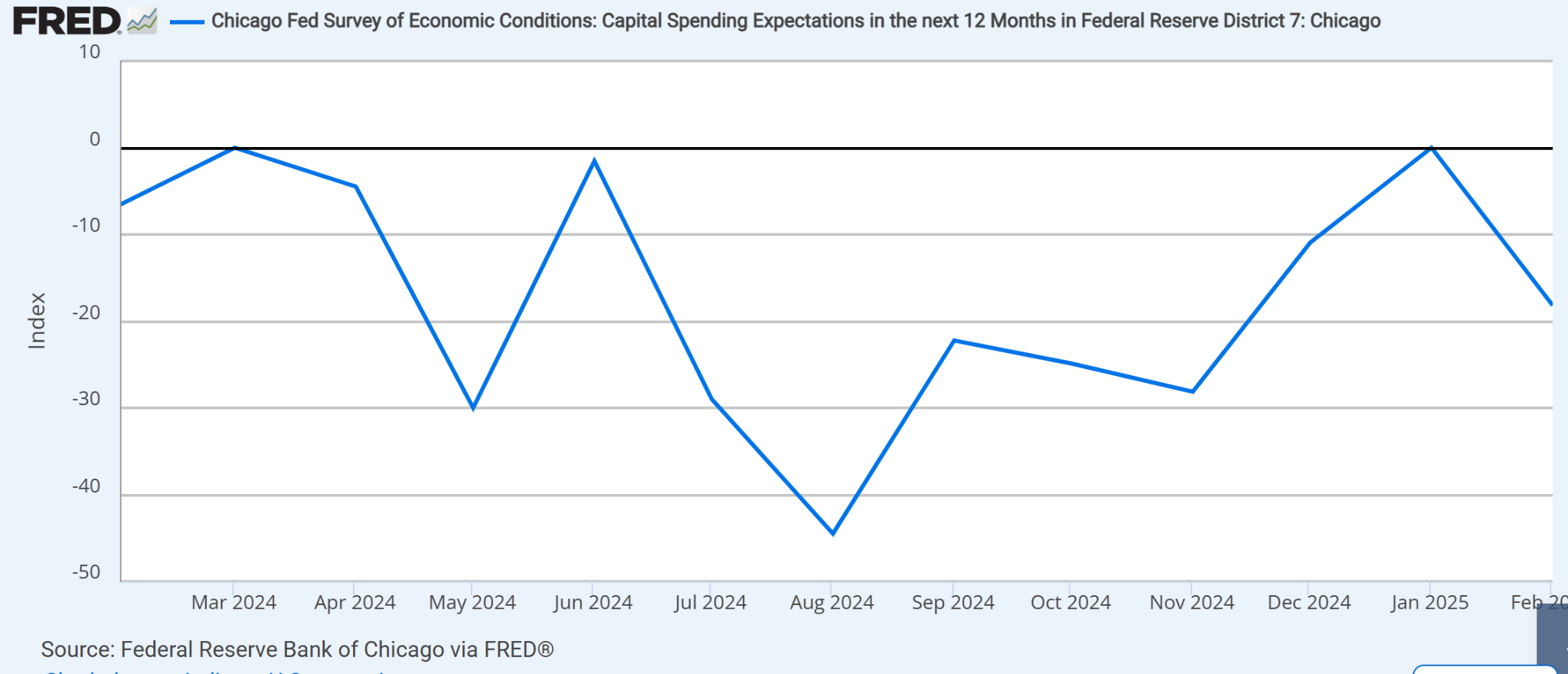

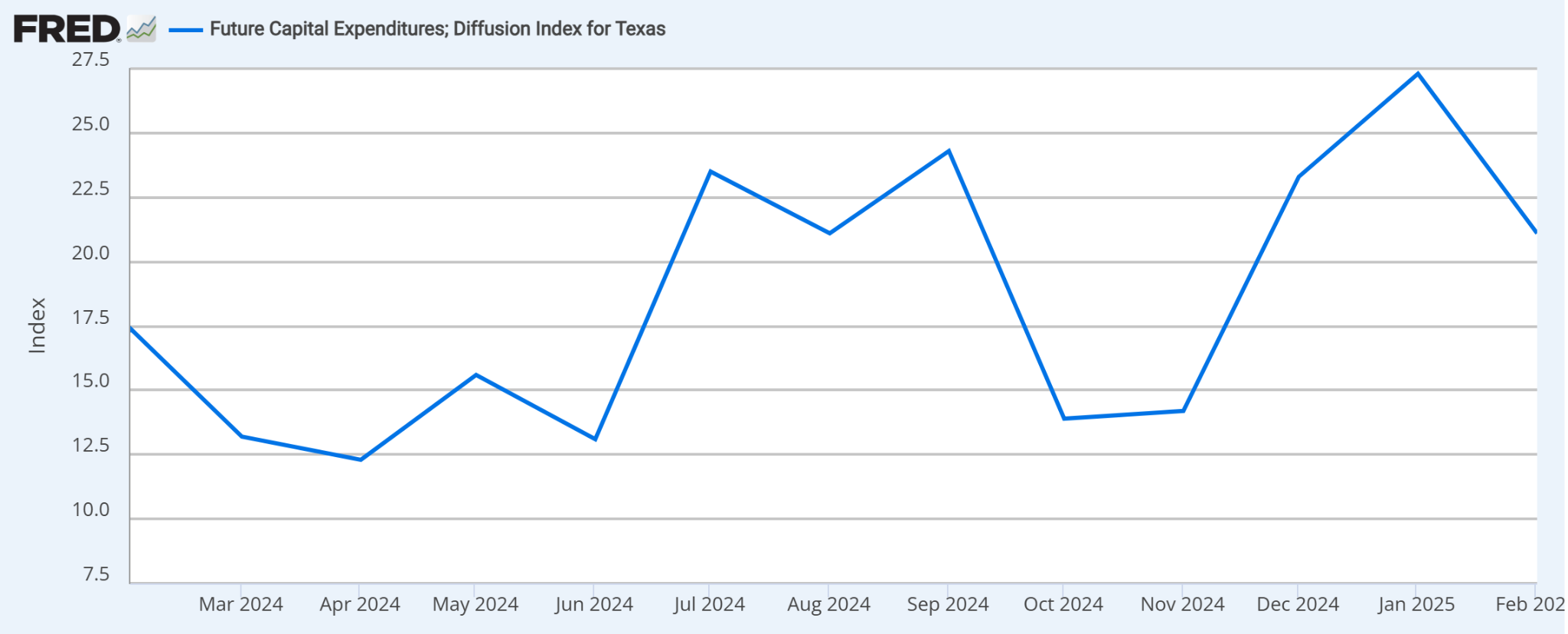

CapEx Spending by Companies is slowing

Below are charts of future capital spending expectations in the next 12 months from four different districts of the Federal Reserve, Philadelphia, New York, Chicago, and Texas. Note the similarities of spending cutbacks. (All pointing significantly lower). If businesses aren’t spending they most likely are not hiring.

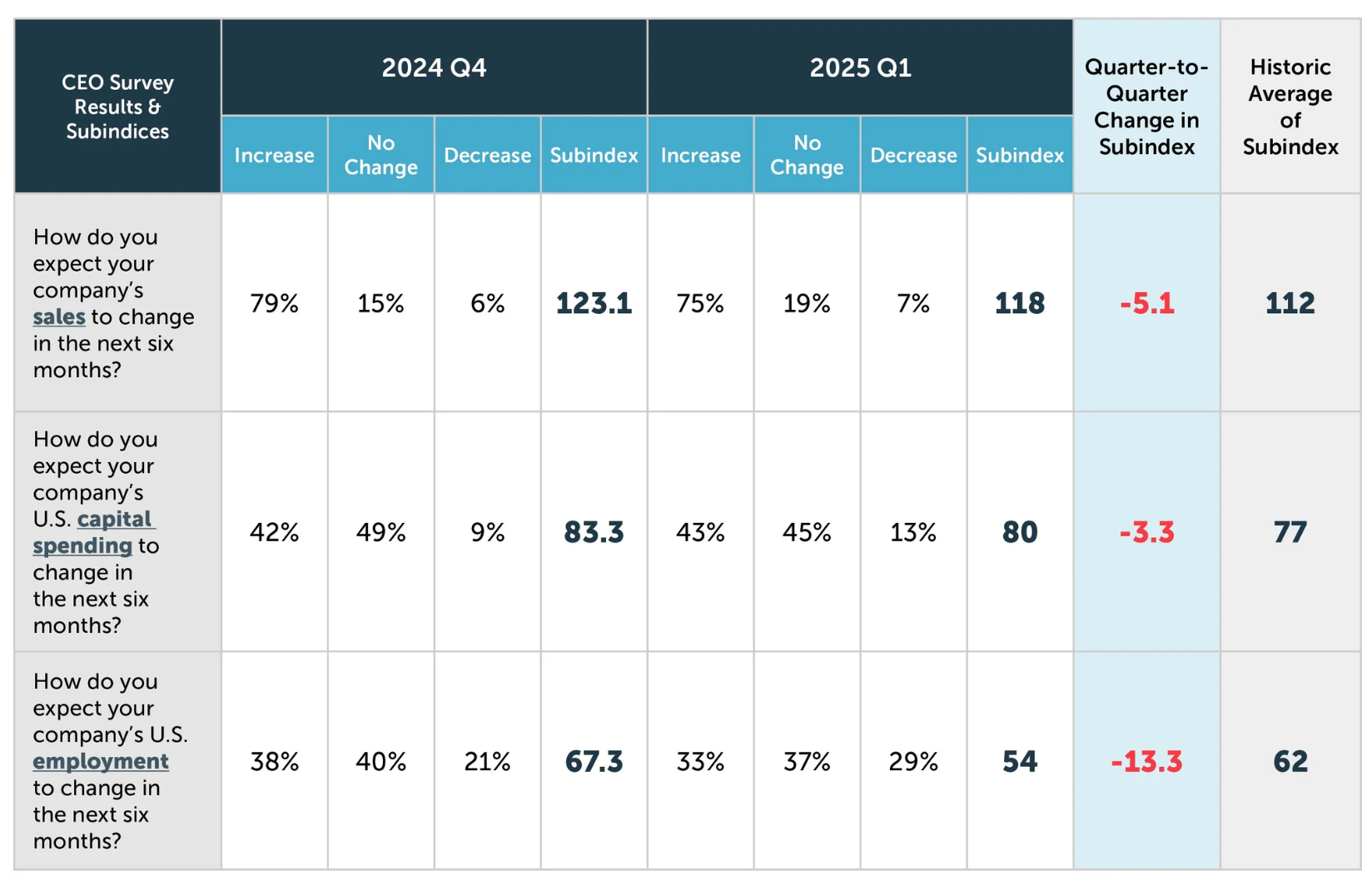

Below is the Business Roundtable

The Business Roundtable is critical to understanding economic activity and consumer sentiment for several key reasons:

Leading Indicator of Corporate Behavior

The Business Roundtable CEO Economic Outlook Index is derived from quarterly surveys of top CEOs, capturing their plans for hiring, capital investment, and sales expectations. Because corporate spending and hiring decisions directly drive job creation and income growth, the survey acts as an early signal of how businesses expect the economy to evolve. When CEOs indicate increased investment and expansion, it often presages broader economic growth, which in turn lifts consumer sentiment.

Direct Influence on Economic Activity

Corporate decisions—such as ramping up hiring or scaling back investments—affect multiple layers of the economy. More hiring means more disposable income for households, which generally results in increased consumer spending. Conversely, if companies cut back, the ripple effect can slow economic activity, dampening consumer confidence. This dynamic makes the Business Roundtable’s data an essential tool for economists and policymakers assessing the health of the economy.

Shaping Policy and Market Expectations

The survey results serve as a barometer not only for business trends but also for public policy. Policymakers and investors closely monitor the Business Roundtable’s outlook to understand the potential impact of regulatory changes, tax policies, or trade tariffs. When CEOs express caution—perhaps due to anticipated policy shifts—this can signal upcoming adjustments in economic policy, affecting both business operations and consumer sentiment.

Feedback Loop with Consumer Sentiment

Consumer sentiment is highly responsive to job market conditions and economic growth. The Business Roundtable’s index offers a snapshot of corporate confidence, which tends to correlate with consumer mood. A robust, optimistic outlook among CEOs generally translates into improved consumer spending and higher sentiment indices, while a pessimistic corporate outlook can signal caution among consumers.

Broad Representation and Credibility

Composed of CEOs from companies that account for a significant portion of the U.S. GDP and employment, the Business Roundtable’s collective voice holds considerable weight in economic discussions. Their aggregated expectations provide a reliable measure of the business community’s outlook, which is a vital input for forecasts of future economic performance.

In summary, the Business Roundtable is important because it connects corporate decision-making with wider economic trends. Its CEO Economic Outlook Index not only reflects the business community’s immediate plans but also provides a predictive tool that helps explain and influence consumer sentiment. This relationship between corporate confidence and consumer behavior is a cornerstone of economic analysis, shaping both investment strategies and public policy decisions.

Below is the table

The survey 3 subindices were as follows:

- Plans for hiring decreased by 13 points to 54.

- Plans for capital investment decreased to points to 80.

- Expectations for sales decreased by 5 points to 118.

This quarter’s survey was in the field from February 19 through March 7, 2025. In total, 150 CEOs completed the survey. More than three-quarters of responses were submitted before the 25% U.S. tariffs on Canada and Mexico were announced on March 3, 2025. Therefore those numbers could decrease even further in the next survey depending on the final decision of tariffs.

Tariffs

Seventy percent of respondents at the Business Roundtable selected keeping tariffs low on intermediate inputs and raw materials, particularly those that cannot be sourced in the U.S. Therefore I expect tariffs to be more of a headline story than reality. YES, there will be new tariffs. But I do not expect tariffs to be anything like what we have seen in the headlines. The headlines from the white house are meant as a negotiating mechanism of masculinity. The headlines news agencies spew are made to frighten to sell additional advertising space. The bottom line I think the final tariffs will be on the GOODS you DO NOT SEE in the headlines. Like sneakers, and textiles from China. Maybe small tariffs on agricultural products from Mexico can be absorbed into supply chains.

The importance of this

When business spending slows significantly so does hiring which leads to a slowdown in economic activity when consumer spending slows so does economic activity. When both slow simultaneously the most likely outcome is slower economic growth in the future. The data has not yet shown up in the hard data but often does down the road. Although, I see a strong possibility of a tradeable market bounce in the short term. I am not yet convinced the market has bottomed.

GDP FedNow report

The Atlanta Federal Reserve’s GDPNow model recently adjusted its first-quarter 2025 real GDP growth estimate downward, from -1.5% on February 28 to -2.8% on March 3, before slightly improving to -2.4% on March 6.

This downward revision was influenced by a significant increase in imports. Data from the U.S. Census Bureau indicates that imports of goods surged by 12% from December 2024 to January 2025, driven by a 33% spike in industrial supplies. This surge contributed to a 27.5% increase in the real goods deficit during the same period.

The widening trade deficit, resulting from higher imports, negatively impacts GDP calculations, as net exports (exports minus imports) are a component of GDP. Therefore, the recent surge in imports has contributed to the GDPNow model’s projection of a contraction in first-quarter GDP.

The 12% month-over-month increase from December 2024 to January 2025 is significant but most likely was caused by purchasing managers getting ahead of possible tariffs in 2025.

Why I feel the worst isn’t over

It was written in Yahoo Finance that approximately 25% of jobs created in 2023 were government jobs And approximately 10- 12% of non-farm payroll jobs created in 2024 were government jobs, this indicates a significant shift in the sources of job growth in the U.S. economy. Rather than robust private-sector expansion driving overall employment gains, a large portion of new positions would be in the public sector. This trend could suggest that:

- Private Sector Slowdown: The private sector may be experiencing slower growth, prompting governments at the federal, state, and local levels to pick up the slack through increased hiring.

- Fiscal Implications: Higher public-sector employment is largely funded by taxpayer dollars and may lead to increased government spending and potentially larger deficits.

- Economic Resilience Concerns: While overall job numbers might look strong, the quality and sustainability of these jobs could differ from those in high-growth private industries such as technology, manufacturing, and services.

- Policy Signal: A high share of government-created jobs might serve as an early warning sign that underlying economic drivers in the private sector are weakening, necessitating policy intervention to boost private-sector dynamism.

In essence, relying heavily on government job creation to drive employment growth may mask broader weaknesses in the private economy, affecting long-term economic productivity and competitiveness.

Anticipating a Stock Market Rebound Amid Oversold Conditions and Easing Tariff Concerns

Recent market dynamics suggest a potential short-term rebound in the stock market, driven by oversold conditions and evolving developments in U.S. trade policy.

Oversold Market Conditions

The U.S. stock market has experienced notable volatility recently, with major indices such as the S&P 500 and NASDAQ Composite entering correction territory. This downturn has led to a significant decline in investor sentiment, reaching levels not seen since September 2022. The heightened economic uncertainty has prompted many investors to reassess their strategies, moving away from traditional “set-and-forget” approaches.

However, periods of pronounced selling can lead to oversold conditions, setting the stage for potential short-term rallies. As Ross Mayfield, an investment strategy analyst at Baird, observed, a market that is down 10% from all-time highs and appears oversold can create favorable conditions for a rally, even if underlying fundamental issues remain unresolved.

Evolving Tariff Policies

Trade tensions have been a significant factor influencing market sentiment. In recent developments, President Donald J. Trump announced adjustments to previously proposed tariffs on imports from Canada and Mexico. Notably, goods from these countries that qualify under the U.S.-Mexico-Canada Agreement (USMCA) will not face additional tariffs. Additionally, certain energy products and potash imports from Canada and Mexico that fall outside USMCA preferences will be subject to a reduced tariff rate of 10%, down from the initially proposed 25%.

These adjustments aim to minimize disruptions to key industries, such as the automotive sector, and reflect a more measured approach to trade policy than initially anticipated. The moderation of tariff measures may alleviate some investor concerns regarding escalating trade tensions and their potential impact on the economy.

Final take

The convergence of oversold market conditions and a more tempered stance on trade tariffs could catalyze a short-term bounce in the stock market. Investors should remain attentive to these developments and consider the potential for a rebound. I see it in a few ways. It could be a tradeable rally. A tradeable rally is a short-term stock rental. Something you don’t want to hold long term. You buy it intending to sell it in a short time. Or a stock you were stuck in presents an opportunity to sell. This stock market and the economy have a way to go before they adjust to the not-yet-in-place new Trump policies. I see a bright future but right now there is quite a bit of fog. That is why I don’t think the worst has yet occurred. If it does happen it will likely occur sometime after a tradeable rally. Staying mindful of the broader economic landscape and ongoing policy shifts makes all the difference between being a winning or losing investor.

And don’t be surprised in 2025 when:

- GDP projections for 2025 are lowered from the current 2.8% to 2% or lower.

- Employment slows to a crawl and Unemployment goes up.

- The 30-year mortgage hits a 12-month low.

- Inflation remains stubborn.

- The Federal Reserve cuts interest rates sooner rather than later, despite stubborn inflation.

- The stock market has not yet bottomed in 2025.

Remember, “I said that”