Between January 20 and January 24, 2025, U.S. stock markets exhibited varied performances across different indices. Here’s a detailed breakdown.

Index Performance

- S&P 500: The index increased by approximately 1.7% during this period.

- NASDAQ Composite: Similarly, the NASDAQ Composite rose by about 1.7%.

- Russell 2000 (Small Cap): The Russell 2000 advanced by 1.4%.

- S&P MidCap 400: The S&P MidCap 400 saw a gain of approximately 1.8%.

MidCap Outperformance and Market Rotation

During this timeframe, the S&P MidCap 400’s performance slightly surpassed that of the S&P 500, NASDAQ Composite, and Russell 2000. While this indicates a modest outperformance of mid-cap stocks, the margin is relatively small. To definitively conclude a market rotation into mid-cap stocks, a more sustained trend over a longer period would be necessary.

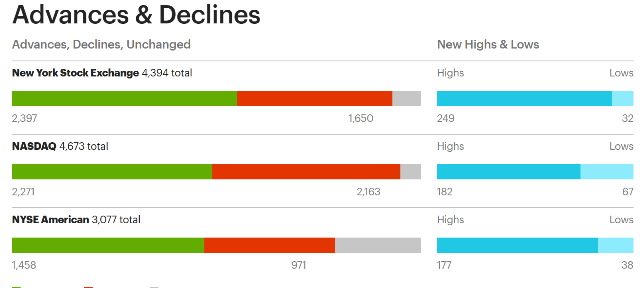

Market Volume and Breadth

On Friday, January 24, 2025, the major indices experienced slight declines.

- S&P 500: Decreased by 0.29%.

- NASDAQ Composite: Fell by 0.50%.

- Dow Jones Industrial Average: Dropped by 0.32%.

Despite these Friday declines, the indices recorded gains for the week. Although a down day, Friday did have a decent showing as advancing issues outpaced declining issues and new stock lows were not increasing significantly. The mixed performance on Friday was attributed to varied economic data and earnings reports. For instance, strong housing market data contrasted with a slowdown in business activity and a dip in consumer sentiment.

Market Sentiment

Investor sentiment during this period was cautiously optimistic. The gains earlier in the week were driven by positive earnings reports and economic data. However, concerns emerged due to mixed economic indicators and uncertainties surrounding upcoming Federal Reserve decisions. The decline in consumer sentiment to 71.1, below previous estimates, also contributed to a more cautious outlook.

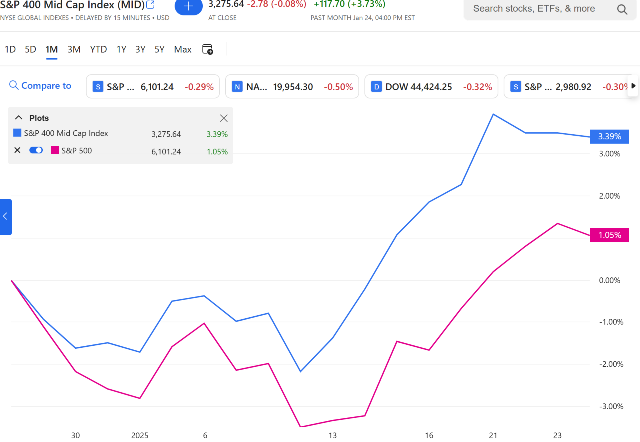

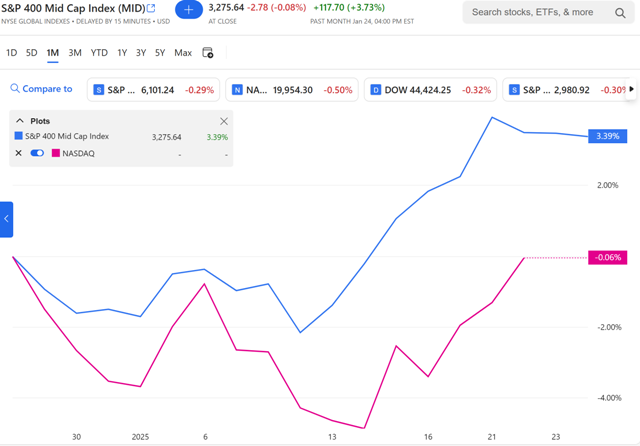

Below are charts of the S&P 400 Midcap vs. the S&P 500 vs. the NASDAQ Comp the last month. Where does it look like the money is rotating?

S&P 400 vs. S&P 500 the last 30 days. (S&P 400 blue line)

S&P 400 vs. the NASDAQ Comp the last 30 days. (S&P 400 blue line)

Below is a chart of the S&P 400 (red) vs. S&P 500 (blue) vs. the Small Cap Russell 2000 (purple)

While I believe that interest rates are likely to decline later this year, it’s important to consider that approximately 40% of the stocks in the Russell 2000 index are unprofitable, with many having variable lending rates. While some small-cap stocks may perform well, small-caps generally have lower liquidity compared to their large-cap counterparts, which can lead to increased volatility. In a market downturn, small-cap stocks are often more vulnerable and could experience significant losses.

Given that large-cap valuations are stretched, many institutional investors are focusing on undervalued mid-cap stocks that are generating profits. Whether you’re a short-term trader or a long-term investor, I believe mid-cap stocks present an attractive opportunity. I have several mid-cap stocks on my buy list.

Conclusion

The marginal outperformance of mid-cap stocks during this period could be indicative of a rotation into mid-cap equities. Many analysts, including myself, have noted that mid-cap stocks, often overlooked between small and large caps, are trading at more favorable valuations compared to the S&P 500 index and are expected to demonstrate strong earnings growth.

However, it’s important to note that while mid-cap stocks have shown strength, the overall market dynamics are influenced by various factors, including economic policies, corporate earnings, and investor sentiment. Therefore, while the recent performance suggests a potential rotation into mid-cap stocks, it is essential to consider the broader economic context when making investment decisions.

What’s ahead?

- Meta Platforms: Usually surprises to the upside, but they announced a major capex expense for 2025 (60 billion). Going to see how the market reacts.

- Tesla: I don’t see things getting better for Tesla in the near term. But Elon Musk is the master of all PR.

- Microsoft: Historically the 4th quarter of a calendar year is strong for Microsoft.

- Apple: Apple has problems in China, but I’m sure the market awaits news on Apple’s intelligence. China and Apple intelligence news will shape the movement of the stock.

- ServiceNow: This company is a beast. But a few analysts have lowered estimates in the past 60 days, and that always worries me.

These reports are expected to significantly influence market dynamics.

Additionally, other notable companies set to release their earnings include:

- Caterpillar

- United Rentals

- General Motors

- Royal Caribbean

Where I see uncertainty among the institutions in the first quarter

As I was cautiously optimistic on the earnings front, that optimism has panned out thus far. The decline in the 10-year note. My call is that tariffs would not be as severe as stated on the campaign trail; a tame CPI and good earnings have shaken off a little of the nervousness. And let’s not forget there is still 5.6 TRILLION sitting in cash. But become short-sighted or too optimistic. I have mentioned several times that if the opportunity presents itself, I will take some off the table for a rainy future day. Earnings season has begun. And thus far, it has been good.

Why be cautious?

I anticipate that inflationary pressures will emerge in both the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) price index, potentially in February or March. These increases are expected to be driven by specific factors, such as rising healthcare costs (particularly health insurance) in the PCE and shelter costs (due to the California wildfires) in the CPI. These are likely to be “one-off” events, but they still have the potential to impact overall inflation data, turn sentiment negative (because interest rates would move higher), and overall trader behavior. (Most likely the short players will emerge.)

Given that the market has settled in the short term, the underlying feeling is already volatile, and stocks are trading at stretched valuations, I believe it’s prudent to take some profits off the table provided the opportunity arises. Market corrections are inevitable, and when this one occurs, it’s important to be prepared. It’s never profitable to look back and think, “I could have, I should have, or I would have.”